Emergency Fund 101 for Freelancers & Creators

Emergency Fund 101 for Freelancers & Creators

As someone building your own business—whether you’re designing, writing, consulting, or crafting digital content—your income can swing from feast to famine.

A robust emergency fund isn’t just “nice to have”; it’s the foundation for confidence, creativity, and long-term growth.

1. Why an Emergency Fund Matters

Smooth Cashflow Gaps: Projects get delayed. Clients pay late. An emergency fund bridges those gaps without stress.

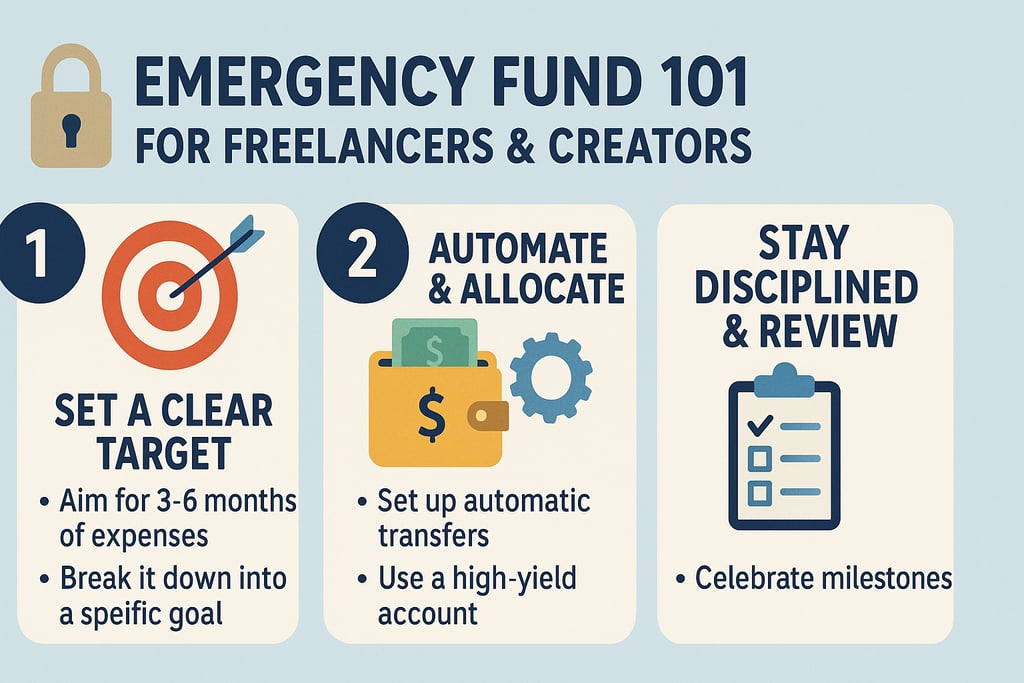

Peace of Mind: Knowing you can cover 3–6 months of bills frees you to negotiate better rates, take creative risks, or pause for self-care.

Avoid Debt Traps: Instead of high-interest credit cards or loans, you’ll have cash on hand.

2. Calculating Your Target

List Essential Monthly Expenses

Rent/mortgage, utilities, insurance, groceries, phone/internet, software subscriptions.

Multiply by Your Cushion

Conservative: 3 months of expenses

Comfortable: 6 months

Adjust for Personal Factors

Health considerations, industry volatility, upcoming business investments.

Example: If your essentials total $2,500/month, your fund should be $7,500–$15,000.

3. Building Your Fund, Step by Step

Step 1: Open a Dedicated Savings Account

Start by opening a separate account specifically for your emergency fund. Ideally, choose a high-yield savings or money-market account to help your money grow safely.

Step 2: Automate Contributions

Set up automatic transfers so that 5–10% of every payment you receive goes directly into your emergency fund without you having to think about it.

Step 3: Use Windfalls Wisely

Whenever you receive extra money—like bonuses, gifts, or tax refunds—direct a portion (or all of it) into your emergency fund to build it faster.

Step 4: Track Progress Quarterly

Every few months, review your emergency fund. Adjust your contribution percentage or savings target based on any changes in your income, expenses, or goals.

4. Smart Strategies to Accelerate Growth

Round-Up Apps: Link your debit/credit cards to round up purchases and deposit the “spare change.”

Side Gigs for Savings: Pick short-term gigs with quick pay to funnel extra cash into your fund.

Tiered Accounts: Keep 1–2 months’ worth in an instantly accessible account, and the rest in a slightly less liquid, higher-yield account.

5. When to Tap In—and When Not To

✅ For True Emergencies: Unplanned medical bills, urgent home/car repairs, or sudden income loss.

❌ Not for: Marketing experiments, equipment upgrades you haven’t budgeted, or “treat yourself” splurges.

Ready to Level Up Your Financial Resilience?

Building and maintaining an emergency fund doesn’t have to be overwhelming. With the right plan, you’ll transform income uncertainty into opportunity—and fuel your creative journey.